Digital mobile payment platform Apple Pay is now available in South Africa, according to several Absa, Discovery Bank, and Nedbank customers. Apple Pay allows users to load a supported banking card and use their Apple device – such as an iPhone or cellular Apple Watch – to make a contactless payment at supported NFC-based terminals.

There have been various signs over the last few months that the service would be coming to banks, including mentions of it on the websites of Absa and Discovery Bank. Numerous MyBroadband forum members and Twitter users on Tuesday morning reported that they managed to load their banking cards to the Apple Wallet and successfully make payments with the service.

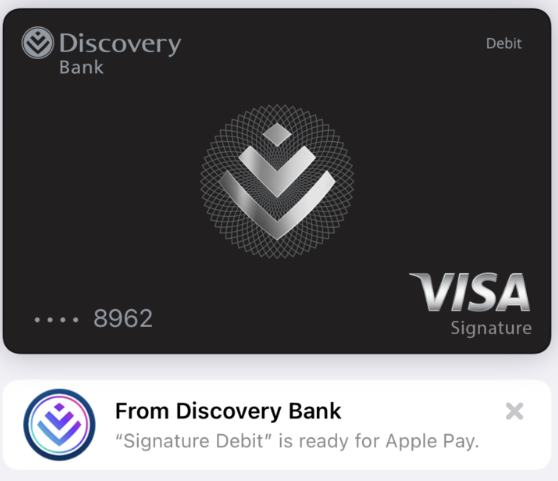

Discovery Bank account holders on the MyBroadband forum started reporting that they were able to use Apple Pay after one user spotted ads from Discovery Bank for the Apple Pay platform on a Google Search. “Managed to successfully add my Discovery Bank card – didn’t need to change region settings,” one user stated.

Users shared screenshots showing the final step in the Apple Wallet process with their Discovery Bank cards successfully added. Two of the Discovery Bank cards confirmed to be supported included the Gold Debit and Signature Debit account cards, as shown in the images below.

Other banking customers reported being able to load their Absa and Nedbank cards as well. “Nedbank Amex and VISA added successfully and managed to use at Seattle Coffee,” one MyBroadband forum members said.

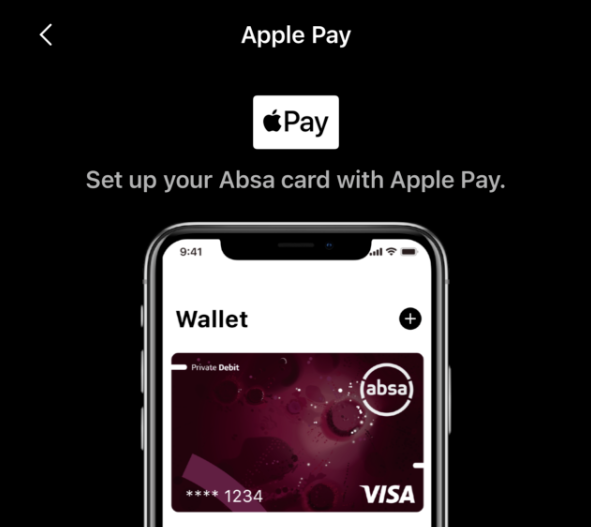

Absa customers also said that they were receiving notifications in the banking app to set up their card with Apple Pay. Below are screenshots of the app notification and a user who successfully activated Apple Pay with an Absa Gold Debit card.

Not available to FNB and Standard Bank customers yet

A number of users indicated that attempts to load any FNB, Investec, and Standard Bank cards were unsuccessful. “I tried FNB Fusion and Credit Cards – both not working,” a MyBroadband forum member said.

“Standard Bank also not working. Guess I’m opening a cheapie Discovery account until all this is resolved,” another stated. An Investec customer on Twitter shared a screenshot showing that he received a “Your Issuer Does not Yet Offer Support for This Card” message.

Comment from banks

MyBroadband contacted Absa, Discovery Bank, FNB, Nedbank, and Standard Bank for feedback on support for Apple Pay.

Absa, Nedbank, and Discovery Bank have confirmed that their customers can now use Apple Pay.

FNB Card CEO Chris Labuschagne said the bank was working with Apple and looked forward to bringing Apple Pay to its customers.

“Once available, it will be accessible at scale to nearly 1 million iPhone users from our 6 million digitally active customers,” Labuschagne said.

Standard Bank did not respond directly to questions over whether it supported Apple Pay.

However, it said that it was “already well engaged with several new payment vendors and partners in order for our clients have access to the most recent digital tap-to-pay services as well as online partner payment systems”.

It added that customers can expect further announcements on this in the near future.